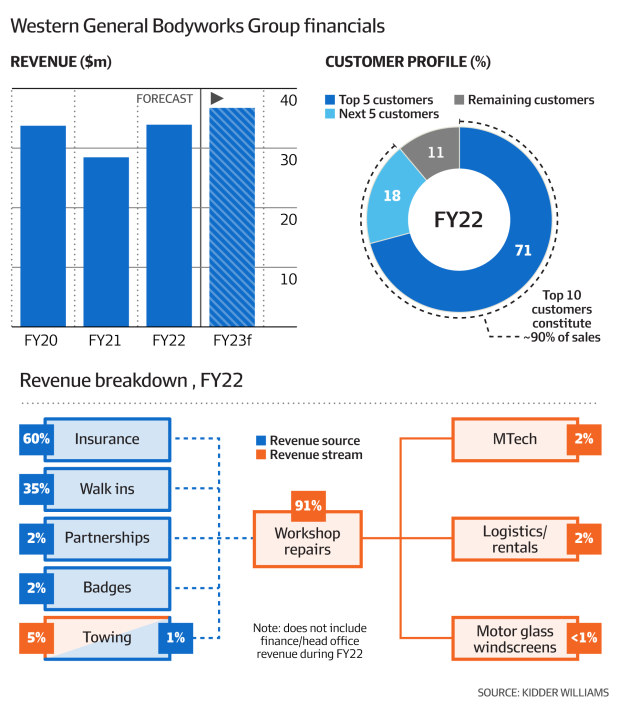

Kidder Williams has pumped the accelerator on a sale process for private smash repair group Western General Bodyworks (WGBW), kicking off talks with private equity funds and other potential buyers.

The accident repairer, based in Victoria, has 11 workshops, more than 170 staff and services north of 10,000 cars a year, according to a flyer shown to potential investors.

WGBW started with one workshop in Maribyrnong and now has 11 sites. Michele Mossop

WGBW was established in 1981 with one workshop in Maribyrnong and now has locations across Melbourne, Geelong (where it is the biggest collision repairer), Newcastle and Gold Coast, repairing cars for insurers including IAG Group, Allianz, Suncorp and Youi.

The group’s owned by businessman Danny Buzadzic, who has 30 years in the vehicle repair industry, and a bunch of acquisitions in the pipeline to try to grow the business and its footprint.

It also recently launched businesses including M Tech Suspension and Motor Glass Windscreen, which provide aftermarket repairs and were said to be on track for positive earnings in FY23. [The businesses were started in the past two financial years].

With all the expansion plans, Buzadzic has hired Kidder Williams to go shopping for a new owner that could help fund it all.

The five-page pitched, sent to potential acquirers this week and seen by Street Talk, looks like a direct call to cashed up PE funds looking for places to deploy their dry powder.

PE funds have sniffed around Australia’s smash repairs sector in the past – Blackstone even had a deal to acquire AMA Group’s panel repairs arm which fell over – with thoughts about consolidating what’s still a fragmented market.

WGBW’s small compared to AMA’s business, and looks like one for the growth funds. It turned over jobs worth $33.9 million last financial year at a double-digit EBITDA margin, the flyer said.

Revenue is heavily skewed towards workshop repairs (91 per cent), and about 60 per cent of its work is insurance jobs.

The flyer said WGBW’s owners were considering their strategic options including a full sale of the business. They hired Kidder Williams to run Project Optimus and test buyer appetite.

The advisers have started drumming up interest, keen to point out that WGBW got through the pandemic better than plenty of its rivals, winning industry awards as the best multi-site operator.

Investment banker David Williams, left, with Tassal CEO Mark Ryan and Cooke Aquaculture chief executive Glenn Cooke, right. Picture: Aaron Francis

Tasmania’s Tassal, the last ASX-listed salmon producer, is looking to expand into new species – including barramundi and kingfish – as it enters new ownership under Canadian seafood giant Cooke Aquaculture.

Cooke settled its $1.7bn takeover of Tassal on Monday – and the company will be pulled off the exchange – with chief executive Glenn Cooke in Australia to meet staff and outline his new operation’s next phase of growth.

This includes exporting Tassal’s products to new markets, including Europe where Cooke has recently acquired a prawn distributor.

“Tasmania sells and I think there is positioning for some of that. I also hope to bring some of our other products through Tassal into the Australian market – shrimp, crab, those types of products,” Mr Cooke said.

The close of the sale marks a transition of Tasmania’s $1bn salmon industry into complete foreign ownership and comes as supermarket chains are looking for more fresh fish meat, particularly white-flesh species, to offer year-round seafood.

Mr Cooke said he would work with Tassal and its chief executive Mark Ryan – who has led the company since 2003 – to expand Tassal’s product offering.

Glenn Cooke, CEO of multinational seafood company Cooke Aquaculture, says he hopes ‘to bring some of our other products through Tassal into the Australian market – shrimp, crab, those types of products’. Picture: Aaron Francis

Cooke has turnover of $2.7bn, with, salmon farms in Canada, US, Chile and Scotland, and 10,000 employees. It is understood to be looking to increase its geographic diversification further to help reduce the risks such as adverse weather and disease.

Mr Ryan said Tassal was exploring expanding into barramundi – four years after it branched out into prawns after it acquired Fortune Group for $31.9m. “(Tassal) doesn’t necessarily have to be salmon and prawns. There’s potential opportunities in barramundi or kingfish,” Mr Ryan said.

“We’re a global operation now. So I think for us, it’s not just saying ‘it has to be here or there’. It really is about which is the best spot to actually do that and give you the best payback and from a risk point, what was going to be the place that minimises the risk.”

Tasmania has also banned further leases of its waterways for salmon farming, pushing producers out into the ocean, about 20km offshore, in rougher, federal waters – or looking to waterways in other states or breeding different species.

Glenn Cooke, left, with Tassel CEO Mark Ryan on Monday. Picture: Aaron Francis

Tassal 40-year-old fish breeding program has delivered a food conversion ratio close to 1:1. In other words, it takes about 1kg of feed to produce 1kg of fish, about eight times less than what’s required to produce the same amount of beef.

Mr Ryan said he was confident it could do the same for other species.

“Prawns or shrimp, globally they work at sort of 2.2-3kg. Already, we’ve taken that down to 1.5kg within three years,” the Tassal chief executive said.

“I’ve talked about barramundi, which is so similar to salmon it’s not funny in terms of infrastructure and practices, and there’s no reason we couldn’t employ that into growing barramundi.

“We’ve got a really good base where we use the technology and particularly the AI where it‘s not just about overfeeding, it’s about underfeeding fish as well. If we can optimise that, that just puts us in a really good spot.”

The company has branched out into seaweed and it hopes to grow the asparagopsis variety, which is used to feed livestock to lower their methane emissions.

Cooke’s acquisition of the company attracted criticism from activist organisations, including the Bob Brown Foundation, which expressed concern that the shift to offshore ownership reduced reporting requirements, while claiming multinationals could buy influence and bully regulators.

Tassal salmon pens at Long Bay.

Mr Cooke dismissed that criticism as “fake news” and a “bald-faced lie” from “well organised groups”. He said science was on Cooke’s side and Tassal had a credible management team.

“We feed a lot of people very healthy protein and we’re going to continue growing our business to more healthy programs. As far as these environmentalists, or so-called environmentalists, you know, we better continue to fight that message with the truth,” Mr Cooke said.

“To basically throw non-truths and fake stories around, bald faced lies, that’s not nice and just discredits them. It just shows what kind of people are out there trying to protest when they have to lie.

“You‘ve got to remember these well organised groups, they have the next platform to get people to scream and yell because they need to raise money to pay for their salaries. So it’s a very circular thing.”

A worker grabs a handful of prawns at Yamba, Tassal’s most southerly prawn farming operation – situated on the Clarence River in northern New South Wales.

David Williams, the investment banker who advised Cooke on the deal through his Kidder Williams advisory firm, told The Australian: “Farming animals and fish has been subject to continuous improvement, in animal husbandry and feed and growing methods.”

Mr Williams was also a previous owner of Tassal, acquiring it for $42.5m after it had fallen into administration in 2003 before floating it on the ASX a year later.

“Modern fish farming is a relatively new business and there are many learnings every year to improve practices. Continuous improvement is important because aquaculture will continue to be a low-cost way of feeding the world,” Mr Williams said.

“Cookes are one of the best operators in the world and will accelerate industry improvement here with their technologies and experience.”

Secret weapon: food and beverage corporate adviser David Williams, who worked with Cooke on the takeover deal. Picture: Arsineh Houspian

Tassal shareholders have overwhelmingly backed a $1.7bn takeover of the salmon producer from Canadian seafood giant Cooke.

It marks the end of a 20-year turnaround at the Tasmanian group, which entered administration in 2002 and was floated on the ASX a year later at 50c a share.

The company will now be removed from the ASX boards later this month after 96 per cent of shareholders voted in favour of Cooke’s fourth and final bid of $5.23 a share on Thursday.

It has been a test of patience for Cooke – which first approached Tassal in 2010 and made its first offer for the company in 2011. When it contacted the board this year, it was armed with a secret weapon: David Williams.

Mr Williams, who runs boutique investment bank Kidder Williams, can say he effectively bought Tassal twice. Once for $42.5m after the group fell into administration and again for $1.7bn after he advised Cooke on the deal.

Tassal chair, former Incitec Pivot chief executive James Fazzino, said it was a “significant day in the history of Tassal”, with Cooke’s bid representing a 49 per cent premium and the “best interests” of shareholders.

His comments came after managing director Mark Ryan – who was appointed as receiver in 2002 and stayed with the company after its listing the following the year – said in August there was no greater external validation than an appropriately-priced takeover bid.

“If you look at a 49 per cent premium, I think it’s a good premium from when it started, and if I look at where we listed at 50c it feels pretty good to get it up to $5.23,” Mr Ryan said.

A court hearing has been scheduled for Tuesday to approve the scheme. If it gets the green light, the takeover will become effective on November 21, with shareholders paid $1.1bn or $5.23 cash a share. The deal also includes about $600m of Tassal’s debt.

It comes after Cooke unsuccessfully made a play for Tassal rival Huon, which was ultimately sold to Brazilian firm JBS for $424m last year.

Cooke has turnover of some $2.7bn, salmon farms in Canada, US, Chile and Scotland, and has 10,000 employees. It is understood to be wanting to increase its geographic diversification further to help reduce the risks such as adverse weather and disease.

Cooke Aquaculture chief executive Glenn Cooke.

Cooke chief executive Glenn Cooke made a direct pitch to Tassal’s 10 biggest shareholders in late June via a phone call described as a “meet and greet”. Mr Cooke told the Tassal shareholders on the call that the company faces limited growth prospects, and under Cooke’s ownership it could take it to the new markets and the next level.

He also gave a summary of Cooke’s history and operations, which includes salmon farms in Canada, the US, Chile and Scotland.

Tassal’s revenue surged 32.8 per cent to $788.7m, while net profit rose 31.9 per cent to $63.7m in the year to June 30.

The takeover comes as salmon prices have eased from a record high. The Nasdaq Salmon Index, which tracks the prices of the fish from Norway, the world’s leading producer, has fallen 5.13 per cent in the past quarter.

But in the past month, prices have crept up again, rising 10.1 per cent. In July, Rabobank said “recessionary dynamics resulting from a decline in disposable incomes” had sparked a shift toward retail from food service.

“For most supplier regions, and especially Norway, supply in (the first half of) 2022 was weak, resulting in a global contraction of 6 per cent, the highest negative supply growth since 2016,” Rabobank wrote in its latest update.

“Salmon supply will improve in 2H, compensating for the supply contraction in 1H. This year’s growth is still the lowest since 2016.”

Canada’s Cooke has signed a $1.1 billion deal to acquire Australian salmon farmer Tassal.

Unperturbed by things like six weeks diligence regimes, bickering over standstills, funding packages, investment committees or the like, the privately owned Cooke brought to a head years of talks with Tassal by making what they thought was their best offer, a $5.23 a share bid.

The unconditional offer, to be paid in cash, came after Cooke acquired a 10.5 per cent stake in Tassal in the past two months, and made approaches at $4.67 and $4.85 a share.

While Tassal rejected the $4.67 and $4.85 a share approaches, Cooke returned for its swansong, which it was confident would be high enough for Tassal’s big shareholders.

Sources involved said there was no need for a heavy diligence regime – Cooke knows the industry as well as anyone, ran diligence on fellow Tasmanian salmon group Huon Aquaculture last year and has had its eyes on Tassal for years.

It was also not reliant on a highly leveraged bid vehicle, a big bank syndicate or pesky LPs to make its purchase, and even had former Tassal owner David Williams of Melbourne firm Kidder Williams in its camp as financial adviser.

Cooke will pay $5.23 a share which was a 49 per cent premium to the undisturbed price, and higher than its earlier bids at $4.67 and $4.85 a share. Tassal last traded at $4.89 a share.

The deal valued Tassal’s equity at $1.1 billion and the company at $1.7 billion, including debt.

It was to be done via a scheme of arrangement.

Cooke already owns a 10.5 per cent stake in Tassal, acquired on-market in trades via a handful of brokers including Macquarie and Canaccord Genuity and under various entities.

Tassal’s the second Australian salmon business to be taken off the ASX-boards in the past two years. Last year it was Huon Aquaculture, the No.2 player to Tassal, which went to Brazilian meat giant JBS after an auction that also involved Cooke.

Goldman Sachs and Herbert Smith Freehills advised Tassal, while Kidder Williams and Allens are in Cooke’s corner.

Tassal announced the deal on Tuesday morning, to coincide with its 2022 financial year results.

A farmer feeds cows for sale for the upcoming Eid al-Adha festival in Indonesia, where there has been a foot and mouth outbreak. Picture: Getty Images

Australia is “behind the eight ball” in trying to prevent an outbreak of foot and mouth disease, following the “decimation” of government-funded animal health programs in the past 20 years.

That’s the assessment of Michael Perich, one of the country’s biggest dairy farmers, agribusiness banker David Williams, and former Victorian premier and livestock vet Denis Napthine.

The trio fear Indonesia’s outbreak of foot and mouth disease will quickly spread to Australia as thousands of tourists return from holidays in Bali.

Mr Perich – who farms 30,000 head of cattle at Leppington Pastoral in western Sydney and is chief executive of ASX-listed food and supplement company Noumi – is particularly concerned about the ability of schools with cows, pigs, alpacas and other cloven-hoof animals to detect and contain an outbreak.

Michael Perich has written to the NSW education department asking it to quarantine students from livestock programs for seven days. Picture: Tracee Lea

Mr Perich – who says he has not seen a government-funded livestock vet on his farm in years – said unlike the varroa mite outbreak that had been contained around Newcastle, it would only take one animal infected with foot and mouth disease to shut down Australia’s multibillion-dollar meat and dairy exports.

“There are a lot of countries that are either foot and mouth disease-free or are in what’s known as a controlled state … and they only buy from foot and mouth disease-free countries,” Mr Perich said. “A lot of them would shut their trading doors (to Australia).”

Shares in Australia’s biggest cattle producer – ASX-listed AACo, which owns about 1 per cent of Australia’s land mass – have fallen more than 18 per cent in the past month to $1.84 a share.

While the company regained some ground on Monday, rising 2.2 per cent, investors are concerned about what an outbreak would do to red meat supply and prices.

Meanwhile, shares in Elders – which hiked its interim dividend this year by 40 per cent to 28c a share, thanks in part to strong livestock pricing – has fallen about 5 per cent in the past week.

Former Victorian Premier and vet Denis Napthine says state-funded animal health programs ‘virtually don’t exist anymore’.

Mr Perich has written to the NSW Education Department to request a ban on student contact with school-based agriculture programs that have farm animals onsite. “We work with schools allowing visits to our farms, plus we donate calves for programs focused around raising dairy calves,” he wrote. “At our farms we implemented last week a 7-day isolation program for any employee or visitor to our farm that has travelled internationally.

“With schools returning back today (Monday), a number of schools have susceptible animals – cattle, buffalo, camels, sheep, goats, deer and pigs – we wanted to ensure that schools are aware of the risk to the $80bn agriculture industry and extreme caution should be taken with any international traveller.”

Dr Napthine – who before entering politics was a government veterinarian who worked on disease eradication programs – said such state-funded animal health programs “virtually don’t exist anymore”.

“The animal health side of the Department of Agriculture has been decimated in the past 20 years. There just isn’t that network of people on the ground,” Dr Napthine said.

“We have got to be absolutely vigilant about preventing it (foot and mouth disease) getting into the country, and the second thing is we’ve got to be absolutely ready to respond immediately if it does get in. On both cases, we’re both behind the eight ball.”

Dr Napthine said the rise of hobby farmers also put the country at risk of a potential outbreak.

Mr Williams, who advises a host of Australia’s biggest agribusinesses, said more government veterinarians were needed.

David Williams says there are not enough government-funded veterinarians to detect and eradicate threats such as foot and mouth disease. Picture Yuri Kouzmin

“And if they are not available then manufacture a solution using vets from private practice, eg from Apiam, one of Australia’s biggest veterinary practices, which is listed on the ASX,” he said.

But he said companies also needed to take responsibility.

“Good corporate governance requires food and ag companies to rate the risks to their businesses. Biosecurity should be one, two and three on that list but rarely are.”

Agriculture Minister Murray Watt announced a $14m fund to ward off the disease, which has reached Indonesia and East Timor.

Australia’s top food and beverage corporate adviser, David Williams bought Tassal from receivership in 2003 before floating the company. Picture: Arsineh Houspian

Canadian aquaculture giant Cooke has swallowed a 5.4 per cent slice of ASX-listed salmon producer Tassal, and is ready to gobble up more chunks of the Tasmanian-based company.

Cooke was revealed as the mystery buyer of a parcel of Tassal shares on Monday after a 10-day spending spree, buying at prices ranging from $3.42 to $3.85 a share and ending speculation that investment banker David Williams was returning for another bite at the company.

Mr Williams bought Tassal from receivership in 2003 before floating the company.

He has brokered some of the biggest Australian agribusiness deals, including turning around the fortunes of almond producer Select Harvests and returning Vegemite to Australian ownership after convincing Bega Cheese to buy the spread from confectionary titan Mondelez.

While Mr Williams was buying Tassal shares last week under Amore Foods – a private company he launched in 2004 – a substantial shareholder notice lodged on the ASX reveals he was purchasing on behalf of Cooke.

Cooke cast a line on Tassal in 2010 before walking home with an empty catch. It later tossed a lure at rival Huon, with Mr Williams advising them on the bid.

Cooke has turnover of some $2.7bn, salmon farms in Canada, US, Chile and Scotland, and has 10,000 employees. It is understood to be wanting to increase its geographic diversification further to help reduce the risks such as adverse weather and disease.

Tassal shares surged 3.1 per cent to $3.97 – a two-year high.

It is understood that Cooke is still active in the market, given Monday’s share jump.

JBS Australia managing director Brent Eastwood said at The Australian’s Global Food Forum this month that salmon farming was a “misunderstood business” and was an efficient way to help meet surging demand for protein.

“At the end of the day the planet we live on, the surface is 70 per cent water. But the protein we consume today is only 7 per cent fish,” Mr Eastwood said. “In many parts of the world there is overfishing of the available natural wild species of fish. But (salmon farming) is a very sustainable business. It’s very energy efficient and doesn’t use much land.”

Tassal chief executive Mark Ryan said at the company’s latest financial results in February that it was now “experiencing the benefits of scale” after completing its investment in salmon biomass growth.

“Together with the investments in and growth of our prawn business, where we achieve more attractive capital and working capital cycles, Tassal is focused on growing cashflow and optimising returns. We have delivered a stepchange in cash generation and believe Tassal is well positioned to deliver further improvements in cash flow and cash conversion going forward,” Mr Ryan said.

“We are now at scale delivering a sustainable annual salmon harvest of around 40,000 hog tonnes, and optimising sales mix through branded product development in retail leveraging Tassal’s No.1 salmon and protein brand position, strategically balancing contract unbranded sales, and capitalising on the strong recovery in global pricing and the commencement of pricing recovery in the domestic market.”

Cooke is being advised by investment banker David Williams, who bought Tassal from receivership in 2003 before floating it on the ASX.

Mr Williams has brokered some of the biggest Australian agribusiness deals, including turning around the fortunes of almond producer Select Harvests and returning Vegemite to Australian ownership after convincing Bega Cheese to buy the spread from confectionary titan Mondelez.

He has been buying Tassal shares in the past two weeks under Amore Foods – a private company he launched in 2004 – on behalf of Cooke at prices ranging from $3.42 to $3.85 a share.

Its shares surged 3.1 per cent to $3.97 – a two-year high – after Cooke’s stake in the company was revealed on Monday. Tassal is being advised by Goldman Sachs as its financial advisor and Herbert Smith Freehills as its legal advisor.

David Williams on his “Fairfield” farm, at Darraweit. Picture: Yuri Kouzmin

It is the middle of Melbourne’s fourth Covid lockdown and the streets of the city’s once-thriving business heart are deserted.

Offices are empty, shops and restaurants are closed and the corporate world is, en masse, working from home.

Except for David Williams.

The ebullient head of his own boutique agribusiness investment firm, Kidder Williams, can still be found in his Collins Street fourth-floor headquarters, eating takeaway from his favourite multi-starred restaurant, The Flower Drum, on the boardroom table, surrounded by a stunning collection of contemporary art and poring over paperwork as he plots his next move.

There is not enough time in Williams’ hectic life for the interruption of a global pandemic.

Not when there are deals to be done, people to talk to, projects to be planned and investments to be made. Even if the networking and schmoozing has to be via Zoom, fuelled with high-end Chinese out of plastic containers.

The much-admired, energetic and quick-thinking Williams, 67, has sat at the heart of many of Australia’s biggest transactions involving food and agribusiness companies for the past 35 years.

David Williams at his office in Melbourne’s CBD. Picture: Yuri Kouzmin

As a trusted corporate adviser, he has rescued leading Tasmanian salmon company Tassal from receivership, helped turn around the fortunes of almond grower Select Harvests, steered Bega Cheese from being a farmer-owned regional business to become a major national food company, convinced global giant Mondelez to sell the iconic Vegemite brand back into Australian hands, and advised governments and farmer co-operatives on how to amalgamate many of Australia’s small statutory authorities, state grain boards and floundering commodity co-operatives into bigger, viable and ultimately saleable businesses.

“I love what I do and I love this industry; I’m passionate about it,” says Williams, who is so omnipresent in his specialist sphere he is often called Mr Agribusiness.

“I absolutely believe in the food and agriculture growth story – and in the aquaculture story – and I’ve been doing this since the 1980s … I sit at this unique intersection of knowledge with capital.

“I know everybody in ag and food, I know their industries, I have the experience and I hear things; if you are a bit of a lateral thinker and have vision, you can then think about what might go with what and put the pieces together before anyone else does.”

And the deals keep coming. Just this year, Williams was central to Bega Cheese’s $560 million acquisition of the Lion Dairy group from Japan’s Kirin, doubling the size and diversification of ASX-listed Bega – which Williams has advised for more than 20 years – to become a $3 billion corporation in one leap.

In 2019 he helped grower-owned Mackay Sugar successfully sell 70 per cent of its shares to German sugar giant Nordzucker for $120 million, and Coca-Cola Amatil divest itself of Shepparton fruit cannery SPC for $40 million.

There has also been advisory work, capital raising and quiet deal wrangling in the aquaculture, timber, nut, sugar and horticultural spaces, with other clients including Select Harvests, Maggie Beer, the Costa Group, Premier Fruits Group and Incitec Pivot.

Just how the colourful, ruddy-faced Williams – a regular raconteur on the business conference circuit where he is jointly wooed and feared for his unpredictable flamboyancy and politically incorrect theatrics – became such a dominant figure in the food and agricultural sector is a fascinating story.

“I don’t have any rural background at all,” admits Williams, with his boyish grin and boundless energy. “I’ve never been a farmer and didn’t come from a farming family.

“But a lot of (food and agricultural) people have paid me a lot of money over the years to learn about their businesses – there’s not a food product I haven’t worked on – so I do know what happens at the back end pretty well.”

Williams’ own upbringing could not be further from that of the traditional Melbourne-based rural company director, who commonly grew up in a wealthy Western District wool squattocracy, boarded at Geelong Grammar, returned home to “the land”, and somehow ended up on the board of Elders, the Wool Corporation or even BHP.

David Williams on his “Fairfield” farm, at Darraweit. Picture: Yuri Kouzmin

Instead Williams’ father, John, was a “ten-quid Pom” post-World War II immigrant. He fled the slums of a gloomy Glasgow as a 21-year-old, after glimpsing an alluring travel poster advertising the blue seas and bikini clad girls of Australia on a sleeting Scottish day.

John Williams worked as a tram driver in Melbourne most of his life. He met Williams’ mother, Olive, a young girl from Mackay working as a conductress at the tramways social club dance. “I like to think I was conceived on a tram,” jokes their son, who was born in 1953, the oldest of six children.

The family grew up in a new cream brick veneer house on a gravel road in Melbourne’s then-outskirts of Ferntree Gully. There were kangaroos, gum trees and galahs. But no car, no holidays and not much money.

School for Williams was Ferntree Gully primary and Boronia High. A bright boy, he didn’t realise his family was hard up until he was chosen to go on a week-long camp at the beach as the poorest kid in class.

“We never felt poor; we had shoes, we ate, and we had our own house,” recalls Williams.

“Dad had a second job as a delivery driver as well as driving trams and Mother wasn’t working until she got a job at the Tupperware factory. But that was our life. I didn’t even know Melbourne Grammar existed in those days.”

Williams’ dad wanted him to quit school at 15, to become a plumber or electrician. Instead Williams chose university; first studying business at Swinburne Tech and then transferring to fledgling La Trobe University, then a hot bed for radicalism – and sex too according to Williams – in the ’70s, where he completed his finance degree, a masters degree in transport economics and got his first job as a tutor.

Few in Australia’s agricultural world know Williams was then employed as a bright up-and-coming lecturer at the University of Sydney, teaching finance and economics, running marathons and practising rugby union for Sydney Uni alongside Australian great Nick Farr Jones.

It was there his connection with agriculture began. He became fascinated by the psychology of companies, and began a PhD study about the capital efficiency of rural co-operatives.

“I looked at why the smallest of co-ops had the lowest labour costs and less bad credit than the big banks and it all came back to psychology, because people in these small country communities knew each other and would know very quickly about any bad debts,” Williams says.

“I was fascinated, in a financial metrics way, about how this sense of community and member behaviour drives efficiency and better financial outcomes, and that led me to study how you harness the strength of a rural co-op to bolster the communities around them, increase the value of farms, and give financial strength to its farmer-members.”

Williams was soon popular on the speaker circuit – even then known for his forthright and funny speeches – as Australia’s co-operatives expert. He always argued that the principles of a pure member co-op should be valued and protected, in an era when many co-ops were financing expansion by selling shares or units to outside investors.

Williams believed the inherent conflict in these arrangements was effectively lighting the fuse to blow them up. It’s an irony not lost on the merchant banker who has watched, and sometimes been part of, the privatisation of some of Australia’s largest farmer co-ops such as Murray Goulburn, Bonlac and Bega Cheese.

But in true Williams-larrikin style, it was an address to the staid World Conference of Finance in Canberra in 1983, supposedly about behavioural economics within companies and co-operatives, that changed his life.

In the midst of a sea of dry economic presentations, Williams’ provocatively titled paper “Male Sexual Arousal and Men’s Model Behaviour” caused something of a stir.

At the end of his talk, the head of Arthur Andersen Australia out of the blue offered Williams, then 29, a job heading the company’s new mergers and acquisitions national division.

Williams had thought his lecturer salary of $38,000 a year was pretty good. The offer of $75,000 a year and an exciting new job in Melbourne was a quantum leap into the corporate world that the boy from the Gully could never have imagined. A decade later he was earning $250,000 plus bonuses.

“And guess what my first job was? The merger of SPC and Ardmona, both co-operatives, in 1984,” laughs Williams. “And 35 years later, here I am demerging SPC from Coke, in between listing it and selling it. It has gone the full circle; the gift that keeps on giving.”

Since then, deals big and small have flowed Williams’ way, following him through successive jobs at ANZ McCaughan Dyson, Hambros, Societe Generale, Challenger and, for the past 15 years, in his own Kidder Williams business.

He has bought state electricity assets worth $1.7 billion for the Americans, worked hand in glove with the Victorian Kennett government in the ’90s in its privatisation of statutory authorities and state-owned assets, helped small rural outfits such as the Geraldton Fishermen’s Co-op survive and go global in its rock lobster sales, worked with multinational companies and kept his regular clients such as Bega Cheese, Select Harvests and Tassal growing and thriving.

Many of his Kidder Williams jobs are simple transactions; cashed-up investors knocking on his door wanting to buy or sell something in food or pharmaceuticals.

But the most rewarding other part of his work is envisaging what deals and strategies, however far-fetched, might be possible and good for his clients.

After conceiving the idea, and convincing his clients and their boards of its potential merits, a passionate Williams – the ultimate rainmaker – then sets out to make the deal happen, including finding the finance to fund it all.

This is when his vaunted “people skills”, bulging contact book, media friends and ferocious networking are invaluable.

“I am good with people … a lot of that comes from being a lecturer,” says Williams. “But being good with people also goes back to having a father who was tram driver, and working after school in a milk bar; you learn how to talk to anyone whether its kids wanting lollies, young mums buying tampons, old Italian ladies, drunks and broken families. And you learn how to serve because they’re your customers.

“It’s like investment banking where you have to be a bit of a chameleon and get on with everyone … The only difference is that, in the Gully, no one ever asked you what school you went to.”

Among the proudest deals he has helped engineer, Williams ranks the popular “bringing-Vegemite-home” plan in 2017. It saw Bega Cheese buy the famous Vegemite brand and other grocery products including peanut butter for $460 million from global Mondelez.

David Williams with Bega Cheese chief executive Barry Irvin. Picture: Stuart McEvoyBega boss Barry Irvin with Australian labelled Vegemite jars in Melbourne.

Williams dreamed up the brainwave with Bega’s executive chairman, and his closest friend of more than 20 years, Barry Irvin. “Barry still thinks it was his idea,” smiles Williams fondly, who then organised the $401 million capital raising to fund the big buy.

In the 30 food and ag deals he does every year, most are mid-market $100-$500 million, often private or family companies.

“Many of these businesses are not listed but built by the most inspiring entrepreneurial types; clients who I respect and love so much I would do the work for free,” he says.

David Williams is standing in his blue flannel shirt in the mist, trying to avoid the cold sheeting rain as he peers over the 2000 hectares of rolling farmland near Wallan, north of Melbourne, he bought four years ago.

Grazing his hills are prized black Wagyu cattle, owned by the well-known Blackmore family who lease the farm and have been tireless in revegetating the land, improving its soils, fencing off the 11km of Boyd Creek that runs through the farm and planting more than 28,000 trees.

Not that Williams aspires to turn the Wallan farm into his plush country pad or spend his retirement years drenching cattle. It’s a consequence of having acquired more wealth than he knows what to do with and his unshakeable belief in the bright future of agriculture and food.

“I’m a simple man, but I’m not really a farmer; I just like the idea of owning land especially when it’s the biggest single piece of land within a 50km radius of Melbourne,” muses Williams.

“It’s not lost on me they are subdividing (new housing estates) five kilometres from here but return on investment is not everything; I just like what Ben and David (Blackmore) are doing with their cattle and their Wagyu business.”

Besides the fees he makes from his corporate clients, Williams has also turned investor himself. It started in 2003 when Williams was advising Tassal before its receivership and no one wanted to buy the failing Tasmanian salmon farming business with its $42.5 million debt owed to ANZ.

“I knew the business so well I said I would buy it myself,” Williams says. “I couldn’t afford it but I wrote a contract (with receivers Korda Mentha) that I would pay the money subject to funding.

“So I wrote a prospectus and in three days, 60 institutions in Melbourne and Sydney I approached had pledged over $100 million; so we floated it but only offered [investors] 80 per cent of Tassal for the $42.5 million. The other 20 per cent was mine; I got it for free.”

Williams, who became Tassal’s chairman and put the new board together with Mark Ryan as its chief executive – he’s still there today – eventually sold his slice for a tidy profit. The company is now valued on the ASX at more than $800 million.

Wallan is not the only farm Williams owns. Earlier this year he pounced on 700 hectares of land for sale for $3 million on the banks of the Derwent River upstream of Hobart. He told The Mercury he had bought the Sorell Creek property – without even visiting because of Covid restrictions – because it might be a good landbank.

Williams in his art-filled boardroom. Picture: Yuri Kouzmin

He has also invested in rural water in Tasmania, laughing that he is now branded a “water baron” by the media (although in true Williams-style, he has been known to turn up at farmer meetings discussing water ownership dressed in a big black hat and with pistols on his thick belt).

Reflecting on his future, Williams says he now wants to play a bigger direct role, pursuing passion projects of his own, pulling contacts together for greater collaboration, and offering free counsel to community groups.

These priorities include encouraging aboriginal groups in northern Australia through the Indigenous Land Council to seize the opportunity to develop and better value their own food brands.

“I think barramundi produced in the Tiwi Islands could be sold to Coles and Woolies, with the extra $1 a kilogram charged to customers going back to communities to build social equity and skills,” he says. “And their brands have an extra value too.” Williams would love to help join the dots.

Another passion plan is to raise $100-$200 million in funds from investors – and his own cash – to plant large scale pecan, macadamia and pistachio tree plantations in northern Australia and the Kimberley, irrigated using the latest water-saving technology from Israel.

Or going full circle and helping farmers set up small producer-led co-ops with a common vision and purpose.

“I know people who’ve got access to land, or to money or the technology and if I put them together I can help make these projects happen; investors are crying out for big scale food projects,” says an enthusiastic Williams.

“We have so many emerging industries and an undeveloped North, but there are just not enough visionaries in agriculture and food in Australia. But one thing I am really good at is selling the dream.”

CLOSE FRIENDS MEAN A LOT TO WILLIAMS.

Paul Thompson, the chief executive of Select Harvests almonds has worked closely with Williams for nine years and counts him as friend.

“He’s gregarious, a born raconteur and likes to be the centre of attention which sometimes makes people think twice about him. But behind all that is a very good operator … a lot of high-net worth individuals hold his counsel in very high regard,” Thompson says.

Select Harvests managing director Paul Thompson.Barry Irvin and David Williams in Kidder Williams headquarters. Picture: Stuart McEvoy

Probably his best-known friendship is with Barry Irvin, the Bega NSW dairy farmer and Bega Cheese boss who he met in 1995. In the past two years they have grown even closer as Irvin has battled, and survived cancer.

Irvin calls his trusted adviser and close mate an unlikely “lifesaver” as he lay in hospital and suffered intense chemotherapy treatments.

“David never let me push him away. He never rang and said, ‘So sorry to hear about your condition,” Irvin told The Australian last year. “Rather he would ring and say ‘What are you doing, you malingering bastard? I am coming to Sydney next week, do you want to have lunch or dinner?’.

“And I would say ‘OK’ because that allowed me to feel normal. It was a means of escape.”

Williams says his insistent invites to Irvin were all about psychological positivity. “My attitude was to continually force him to think he is coming back.”

ARTISTIC FLAIR

Contemporary art is Williams’ other deep passion beside his work and his family (he has two adult sons). He says it’s not really an investment – he buys what he likes.

His Melbourne office where his 10 staff work is jam-packed with big colourful artworks.

“I like to pick artists early before they are known – people like Graham Sydney and Roche – and support them,” says Williams, as he excitedly highlights his collection of risqué Chinese cartoon art, aboriginal burial poles, mesmerising red-eyed New Guinea mudmen and his newest painting by Mexican artist Francesco Toledo, which he just bought for $1.3 million.

Then there’s the notorious mating cow sculpture by John Kelly at the reception desk, made famous on national TV when Williams suggested the front black-and-white cow represented Australian dairy farmers and the back cow was Woolworths. (The artwork is no longer featured on Kidder Williams’ website after staff at a major client questioned which symbolised them).

David Williams with his controversial art. Picture: Yuri Kouzmin

If work, family and art are Williams’ public obsessions, his generosity to artistic institutions such as the National Gallery of Victoria and the Australian Ballet is less well known. So too is his family’s quiet support for more than a dozen charities, his favourite being IMPACT which supports women and children escaping domestic violence.

FORECASTING FOOD’S FUTURE

One of the reasons David Williams is so respected within Australia’s food and agribusiness industry is that he has an uncanny knack for predicting the future; for seeing the shape of things to come before anyone else.

It has made his annual, and often contentious, predictions delivered at the close of the prestigious annual Global Food Forum an unmissable event.

Investors, chief executives, bankers and board members of some of Australia’s biggest agribusinesses and listed food companies hang on his every colourful word.

This year was no different. Although Melbourne-based Williams was absent from the Sydney 2021 GFF event in early June because of a snap Victorian Covid lockdown, his prescient observations were published in The Australian the following day and attracted their usual chorus of admirers and devotees, keen to pass on his words of wisdom to their own board of directors and executive teams.

Williams warns that the food and ag industry we knew in 2019 is gone and is never coming back.

“Try as companies might to recreate the success of years past, there is a new normal, and it has changed the industry forever. Think QR codes, think distancing, think vaccines. Many companies have not acknowledged a permanent change and are unprepared,” he says.

“Take an example of a farmer, how will he pick his produce if international travel continues to be limited; the fruit on the vine over several seasons will be well and truly spoiled by the time backpacker labourer return.

“If we could have planned (for a pandemic), we would have thought increased mechanisation, new varieties, protected cropping, new geographies, and new labour models.

“But we didn’t see the need for planning and I fear many still do not. Yet the benefits in planning, instead of just responding, have been highlighted, both in government and in the way we run our businesses.

“There needs to be a new way forged, and company boards need to understand why we are never going back and then embrace what has just happened and a new future.”

Recognised as one of the most influential figures in Australian agribusiness, David Williams is the force behind some of the industry’s most profitable deals.

He is the man who helped transform Bega Cheese into a national food heavyweight; the one who rescued Tassal salmon from receivership; and the saviour who reversed the fortunes of once-flailing almond grower Select Harvests.

How he built this enviable position – as the ultimate rainmaker who can see what the future holds for food and drink before anyone else – is a story as entertaining as the man himself.

Find out how Williams cemented his reputation as Australia’s Mr Agribusiness in AgJournal, free with The Weekly Times next week.

You must be logged in to post a comment.